January Newsletter

Welcome to the first newsletter of the CODE project!

This first newsletter marks the first anniversary of the CODE project. It has been an exciting year. I – Antonio – as the principal investigator, developed the programme on Geopolitics and Technology at CSDS, worked on the theory and research design of the project and hired the first three researchers: Mahmoud, Riccardo, and Thao. By the way, we are also looking for a postdoc to join the team. The call for applications can be found here.

Since September, the team has been busy defining the research objectives and collecting data on patents and market indicators that we will use to measure technological competition. We are also preparing an elite survey, a database on technology agreements and an event to launch the Geopolitics and Technology Forum here in Brussels.

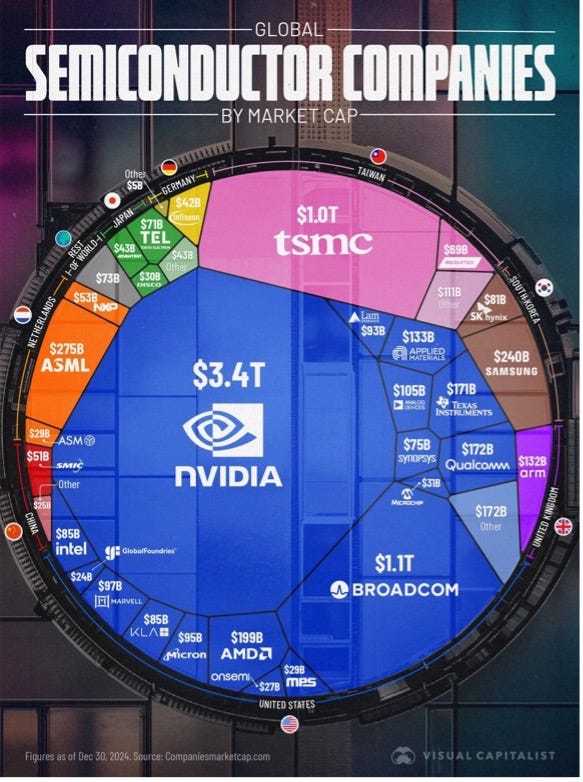

The purpose of this newsletter is to report on some interesting news that has happened over the last few weeks. Today, I would like to start with an infographic circulated widely in my network, which measures the value of the entire semiconductor value chain. According to this chart, American companies account for 71.5% of the industry's global market capitalisation, even though most advanced chips are not actually produced in the United States but in Taiwan, showing the outstanding importance of design capabilities for this industry.

Source: Visual Capitalist

Much has been said recently about the effectiveness of export controls. I would like to refer you to two thought-provoking articles on the subject, one by Scott Kennedy in Foreign Affairs and the other by Paul Triolo in the American Affairs Journal. On the one hand, they have damaged China's ability to develop AI systems, for example, by blocking the purchase of Nvidia's graphics processing units (GPUs). On the other hand, they didn’t prevent China from remaining a leader in electric vehicle batteries and green technologies in general and have actually boosted Chinese domestic investment in the most advanced areas of semiconductor equipment and tools. The key question is: would China have invested so much anyway? Probably yes, but US export controls may have turbocharged it.

The most important consequence of export controls, as Paul Triolo writes, is that they have forced Huawei to transform itself from a hardware company into a hybrid hardware-software giant, seeking greater independence from the United States throughout the industry's supply chain. Triolo writes: "Across the board, Huawei has demonstrated a comprehensive and evolving approach to meeting its semiconductor needs, and these efforts may be paying off”.

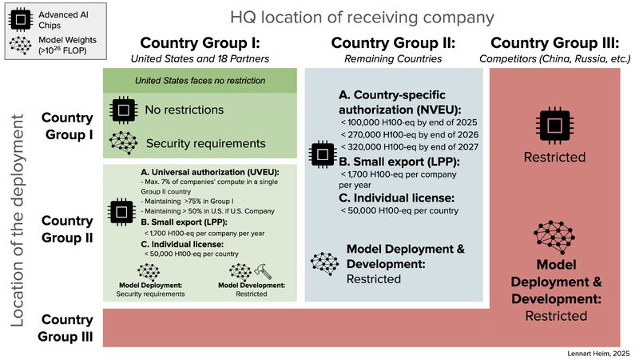

The timing is probably no coincidence, but the Biden administration has just imposed extensive controls on the export of chips used in artificial intelligence. The interesting thing is that the US has created a three-tier licensing system for chips used in AI. The first tier (which includes members of the G7 and key US allies in the Indo-Pacific and the Netherlands) will be unrestricted, while the third tier (which includes China, of course) will be entirely restricted. Let's see if Trump continues with this policy or if he changes the countries included in each list (or even threatens to downgrade them if they don't conform to US preferences).

Source: Lennart Heim

In another sign of US-China technological and geopolitical competition, the US Department of Defence has just blacklisted CATL, the world's largest EV battery maker, China's tech giant Tencent and Cosco, one of China's largest shipping companies, for alleged links to the Chinese military. They won't be able to sell products to the Pentagon, but for now, CATL can continue supplying US companies, including Musk's Tesla (more on him below). We expect these companies to take legal action to challenge the decision (Xiaomi successfully challenged its inclusion on the 2021 blacklist).

Speaking of Elon Musk, in the country I come from (Italy), almost the only thing anyone is talking about is the ongoing talks for an alleged agreement between the Italian government and SpaceX for a 1.6 billion contract for the Starlink service. For the optimists, this cooperation could help consolidate transatlantic relations, given the positive relations between Musk and Meloni (and between the latter and Trump); for the critics, there would be problems linked to excessive dependence on an unreliable partner like Musk. Some time ago, together with Giovanni Tricco, I wrote an article that extended the question to the European level, trying to understand how to reconcile technological competitiveness with economic security (and explicitly referring to Starlink).

Starlink's main European rival, IRIS2, has just been launched and will be operational in 2030 (if all goes well). Given Europe's Ariane launcher delays, Europe is already using SpaceX rockets to put European satellites into orbit. Europe's desire to distance itself politically from Musk may clash with the reality that Europeans are still far from having a reliable alternative.

I would like to point out two academic articles: the first, published in the Journal of International Economics, examines today's fragmentation of trade and investment along geopolitical lines and compares it to the early years of the Cold War. The second article, published in Perspective on Politics, considers how digital platforms use their role as gatekeepers in two-sided markets to consolidate their influence and tests this argument in the case of Apple. A theoretically sophisticated argument demonstrated how the literature on corporate power can be utilised to understand significant economic and geopolitical dynamics. This is what our project aims to contribute to.

In terms of books, I'm currently reading “The NVIDIA Way”. This follows my completion of "The ASML Way”, a truly brilliant story. It was so engaging that I finished it just in two days. One who talks about innovation and industrial policy should read it to understand what works and what doesn't and how difficult it is to be competitive in the digital age. European industrial plans in the 1980s and early 1990s helped ASML's development. Still, the key was for the Dutch company to establish virtuous links with non-European partners, such as the Taiwanese, to gradually specialise in an essential component of the semiconductor value chain, i.e. lithography machines. Partnerships with other European companies, such as the German optical technology specialist ZEISS, proved crucial. There are lessons to be learned for today’s challenges. Finding a balance between European cooperation and openness to global markets (and resisting protectionist tendencies) could be a good strategy for remaining (or returning, or finally becoming) relevant in the digital age, reducing European productivity gaps, and ensuring the indispensability of the European industry of today and tomorrow.

You may have noticed that I am passionate about company stories by now. So, I will end by recommending the book “Samsung Rising”. Just excellent.

On to the next one!